In Q1 2026, GCash processed 4.4 billion transactions, while Maya closed the same quarter with 5.3 million monthly active borrowers on its digital bank books. Two super-apps. One Filipino consumer. A regulatory clock that just got louder.

The Duopoly Is Real, and So Is the Squeeze

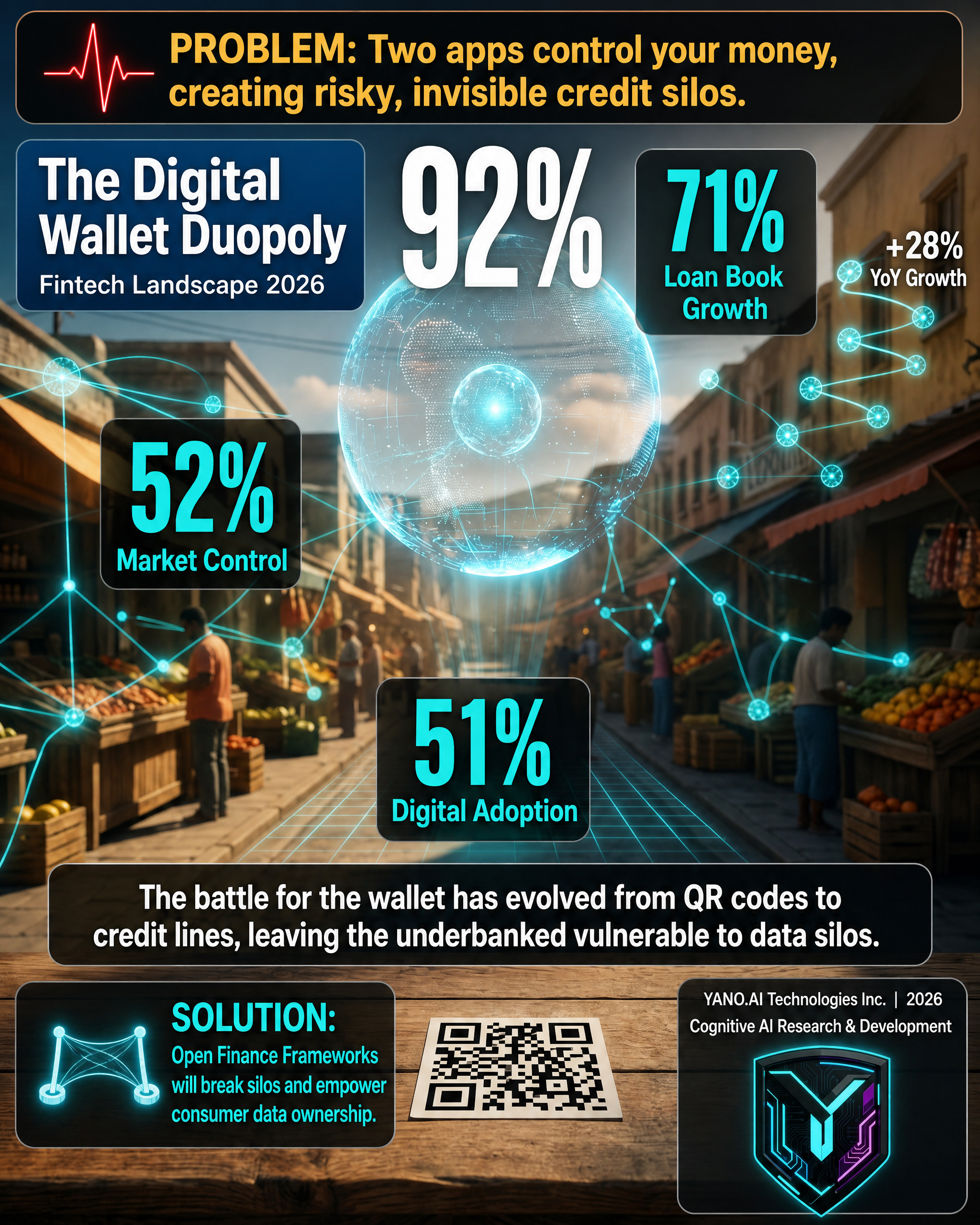

Maya now holds roughly 50% of the Philippine e-wallet market by monthly active users, with GCash trailing close behind at 42%, according to data published by Statista in early 2026. The remaining 8% is split across a long tail of niche wallets, neobanks, and traditional banks scrambling to keep their own apps relevant.

That concentration has consequences. Two players absorb most of the new account growth, most of the merchant onboarding, and most of the consumer trust. A small sari-sari store owner in Cebu now has to choose which QR code to stick on her counter, and which one's settlement fees she can actually stomach.

The Bangko Sentral ng Pilipinas (BSP) reported that digital wallet transactions hit PHP 3.8 trillion in 2025, up 28% year-on-year. That is not a niche product anymore. It is the rails.

Where the Money Actually Moves

The growth story hides a quieter shift underneath. Maya's pivot from e-wallet to digital bank, completed in 2023, is paying off in credit, not payments. Its loan book grew 71% in 2025, according to the company's investor disclosures, with most of that exposure sitting in short-tenure, high-frequency products like Pay Later and personal cash loans.

GCash responded with GSave, GCredit, and a deeper partnership with CIMB for deposits. The race moved from "who owns the QR" to "who extends the credit line."

That move matters because the Philippines remains underbanked. The BSP's 2025 Financial Inclusion Dashboard still places roughly 51% of adults outside the formal credit system. Fintech fills the gap, but it fills it on its own terms, with its own risk models, and with very little public data on default rates among the unbanked.

The Cost of "Free"

Most consumers think sending money between GCash and Maya is free. It usually is, up to a point. The moment a transaction crosses a threshold, or hits a wallet-to-bank transfer, fees show up, often quietly.

GCash charges PHP 15 to PHP 25 for cash-in via over-the-counter partners, depending on the channel. Maya's bank transfer fees scale with destination bank and amount. The "free" in fintech-PH is a marketing choice, not a structural one.

The cost of merchant acquiring is even more revealing. GCash's standard QR merchant fee sits around 2.5%, while Maya's negotiated rates can dip below 1.5% for high-volume retailers, according to industry coverage by Disrupt Asia in late 2025. For a small merchant doing PHP 200,000 in monthly volume, the difference is PHP 2,000 to PHP 4,000 in pure margin.

That is rent paid to the platform. Every month. Without a lease.

The Regulation Question

The BSP's Digital Payments Transformation Roadmap set a target: 50% of retail payments digital by end of 2025. As of the latest published data, the Philippines crossed 52%. The roadmap delivered.

What comes next is harder. The BSP's Open Finance Framework, which took effect in stages through 2025 and 2026, is supposed to let consumers share their bank data with licensed third parties. In practice, the country's two biggest e-wallets hold most of that data inside their own closed loops.

The same pattern is showing up in the credit space. The BSP's move toward a unified credit information database is moving slowly. Until it lands, fintech lenders are effectively scoring borrowers in silos, with each platform holding a partial view of the same person.

The risk is obvious. A borrower can carry four credit lines across four platforms, and none of them know the others exist. Until they default.

FAQ

Q: Is GCash or Maya bigger in the Philippines right now?

A: Maya leads in monthly active users at roughly 50%, with GCash close behind at 42%, according to Statista's 2026 market share data. The two together control about 92% of the e-wallet market.

Q: Can I send money from GCash to Maya for free?

A: For small amounts, yes. Once you hit certain thresholds, or when transferring wallet-to-bank, fees of PHP 15 to PHP 25 typically apply, depending on the channel.

Q: Are Filipino fintech lenders regulated?

A: Yes. The BSP supervises digital banks, e-wallets, and lending platforms. Open finance rules and a unified credit database are still rolling out through 2026.

Q: What is the Open Finance Framework?

A: It is a BSP rule that allows licensed third parties to access consumer financial data with consent. The goal is to break the data silos built by individual super-apps and traditional banks.

Key Takeaway

The next chapter of Philippine fintech will not be won on QR codes. It will be won on credit, data, and trust, and right now, two platforms are holding most of the cards. If you are a small merchant, a borrower, or a founder building in this space, the real question is which platform's rules you want to live inside.

Sources

Sources — external references open in a new tab.